Succession Planning

Succession Planning

Deciding who should take over your business when you retire is something all owner managers have to address at some point. But succession planning is all too often overlooked until that day approaches.

It may be that you’d prefer to keep the business in the family, passing it on to the next generation, who might already be involved in its running. Or you might like to reward your managers for all their loyalty and hard work by selling it to them in a management buy-out.

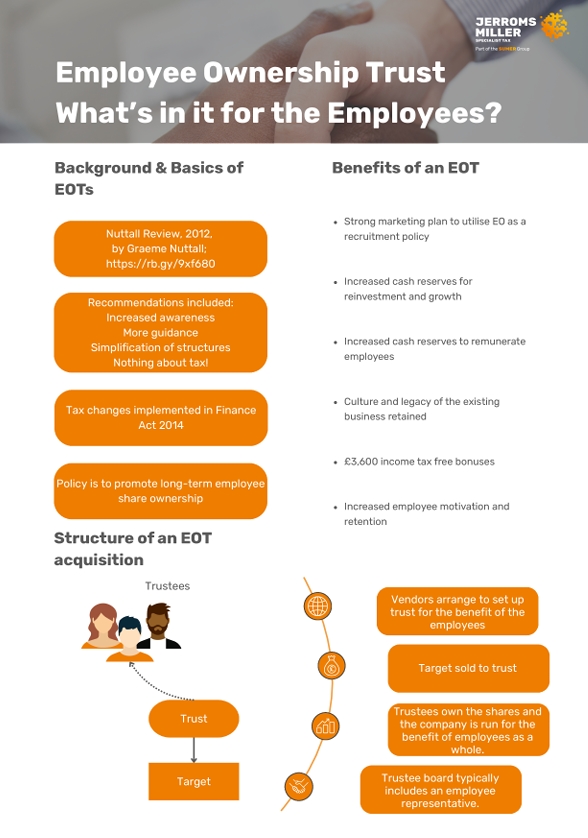

Alternatively, you could dispose of your controlling ownership to an outside buyer in a management buy in – or sell the entire business to another company or individual. Or you could go down the increasingly popular Employee Ownership Trust (EOT) route, giving your employees control of the business and a say in its future.

Considering the options

There are several different options to consider, but whichever you choose, you should start your succession planning early. It’s important you seek sound professional advice so your exit is structured in a tax efficient way.

If you’re selling your business to a third party, don’t delay your marketing. It typically takes more than a year to complete a sale, so prepare to put it on the market and get ready for due diligence as soon as possible. You’ve worked hard to build your business so you’ll want to make sure you reap the rewards when you eventually relinquish control.

.png)